The Dual‑Triangle Model: How AI Reshapes Restaurant Demand and Career Value — and ICC’s Strategic Position

- ICC

- Feb 4

- 7 min read

AI, automation, and robotics will not “eliminate restaurants,” but they will reallocate where human labor creates (and captures) value. In mass‑market dining, rising labor and compliance costs accelerate the shift toward standardization, process engineering, and chain‑level operating systems. In premium dining, differentiation increasingly concentrates in human‑dominant capabilities: taste judgment, craft, aesthetic composition, service pacing, cultural storytelling, and organizational delivery.

This paper proposes a Dual‑Triangle Model: (1) a Market‑Demand Pyramid in which consumption volume concentrates at the bottom (low‑end dining), and (2) a Career‑Value Inverted Pyramid in which high‑quality career and entrepreneurship value concentrates at the top (premium dining). The central thesis is simple: market volume concentrates downward while career value concentrates upward. ICC’s strategic role is to become an enabling infrastructure for the “upward concentration” side of the equation—by professionalizing Chinese cuisine through standards, training systems, and credible honors (e.g., Blue Banner).

Keywords: restaurant automation, chainization, culinary professionalization, premium dining, Chinese cuisine talent, certification, Blue Banner

1. The Core Thesis: “Scale” and “Value” Are Decoupling

Restaurants will remain essential because people will continue to eat. But how restaurants operate—and what it means to build a career in restaurants—is being rewritten by cost pressures and technology adoption.

Two signals matter:

Cost structure hardening (especially in high‑cost regions): California’s fast‑food minimum wage changes require covered fast‑food restaurant employees to be paid at least $20/hour starting April 1, 2024, and the law also establishes a Fast Food Council empowered to set future standards.

Independent operators under compounding pressure: The James Beard Foundation’s 2025 Independent Restaurant Industry Report (in collaboration with Deloitte) characterizes 2024 as a year marked by rising labor costs, economic headwinds, and extreme weather events.

These conditions do not imply “restaurants are dying.” They imply operating models are bifurcating: mass‑market dining moves further toward industrial logic; premium dining becomes more dependent on professional human talent and complete experience design.

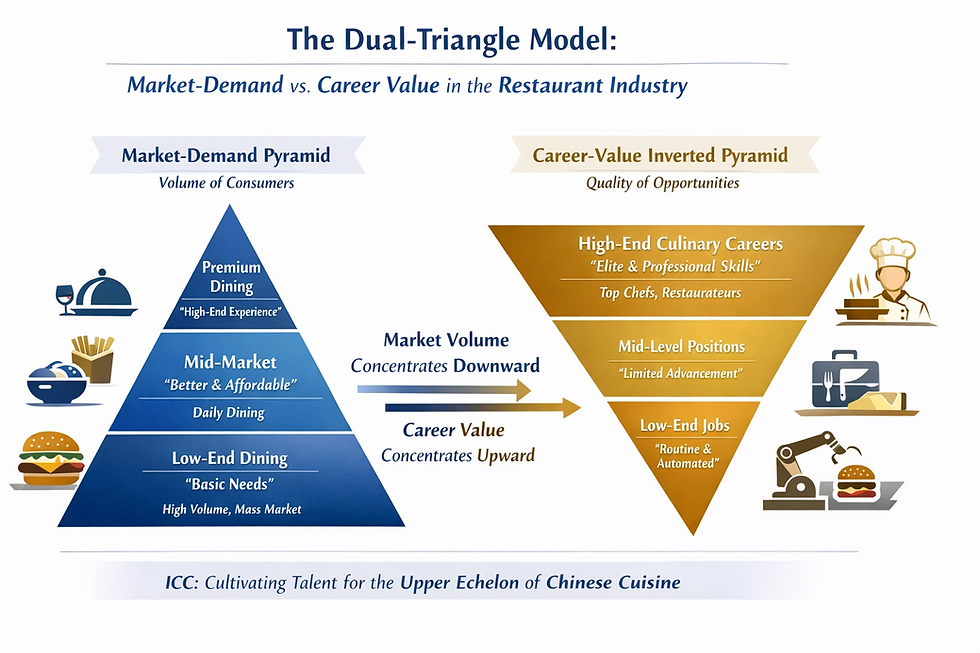

2. The Dual‑Triangle Model

2.1 Triangle #1: The Market‑Demand Pyramid (Volume)

From the consumer side, restaurant demand naturally forms a pyramid:

Base (Low‑end dining): Largest population base and highest frequency—primarily “feed me reliably and affordably.”

Middle (Mid‑market): Upgraded daily dining—“better taste, better setting, reasonable price.”

Top (Premium dining): Smaller audience and lower frequency, but higher willingness to pay for aesthetic, social, cultural, and ritual value.

This is intuitive and stable: most people eat daily; fewer people spend premium prices frequently.

2.2 Triangle #2: The Career‑Value Inverted Pyramid (Quality of Opportunity)

From the labor and entrepreneurship side, what matters is not just “jobs,” but career‑quality opportunity density—the concentration of roles that provide:

skill‑based wage premium and bargaining power

clear advancement pathways (chef → sous chef → head chef → executive chef → partner/operator)

compounding returns (reputation, signature style, team systems, brand equity)

resilience against platform rules, price wars, and pure cost competition

meaningful authorship (craft + aesthetics + storytelling)

Under that definition, the pyramid tends to invert:

Low‑end dining: high headcount potential, but lower career‑value density because tasks are easier to standardize and automate.

Mid‑market: the most crowded and vulnerable zone—often lacking both scale advantages and true experiential differentiation.

Premium and upper‑mid dining: fewer venues overall, but highest density of professional roles where skill and taste judgment remain central and compounding is real.

2.3 The Thesis in One Line

Market volume concentrates downward; career value concentrates upward.This is the structural reason ICC should lead the narrative about professionalization and premium‑capability formation in Chinese cuisine.

3. Mechanisms: Why Low‑End Dining Becomes Less Career‑Friendly Over Time

3.1 The Low‑End Operating Optimum = Systems + Standardization + Scale

When the competitive goal is “faster, cheaper, more consistent,” the winning architecture resembles a retail fulfillment system:

process decomposition (prep → portioning → assembly → handoff)

SOPs and audits

supply chain engineering

automation modules where ROI is clear

digital ordering pipelines and production planning

A highly visible example is Chipotle’s restaurant‑environment testing of “cobotic” devices:

Autocado cuts, cores, and peels avocados before they are hand‑mashed for guacamole; it was operating at a Huntington Beach, California location, and the Augmented Makeline was used at a Corona del Mar, California location.

Chipotle explicitly frames this as part of a stage‑gate process and describes the next steps as optimizing systems and gathering crew/customer feedback before broader pilot plans.

Chipotle notes Autocado takes ~26 seconds on average to process an avocado’s fruit.

The significance is not “one machine.” The significance is that a leading chain is systematically extracting human labor from low‑value, time‑consuming prep tasks—and reallocating staff toward other activities.

3.2 Automation Diffusion Is a Capital Trend, Not a Meme

Robotics adoption is not confined to restaurants, but restaurants are part of the broader service‑automation wave. The International Federation of Robotics reports that professional service robot sales reached almost 200,000 units in 2024 (+9%), with staff shortages cited as a key driver.

This supports a practical expectation: automation modules will continue to appear where they improve throughput, consistency, and safety.

3.3 Chainization: Scale Players Continue to Expand Their Footprint

Technomic’s Top 500 Chain Restaurant Report highlights that location development continued to lift Top 500 performance, with the domestic footprint expanding to 236,000+ restaurants.

This matters because system players have built‑in advantages:

procurement and distribution leverage

repeatable store development

centralized training and compliance

capital budgets for tech trials

data and loyalty systems

brand acquisition and traffic stability

For low‑end independent entrepreneurs, the competitive set increasingly includes system‑optimized chains, not merely neighboring independents.

3.4 “Activities” vs. “Jobs”: Why Skills Get Compressed at the Base

McKinsey Global Institute’s automation research emphasizes a critical nuance: few occupations are fully automatable, but many contain automatable activities. MGI notes that while less than 5% of occupations can be automated entirely using demonstrated technologies, about 60% have at least 30% of activities that could be automated.

Low‑end restaurant work contains a high share of repeatable activities (portioning, assembly, predictable prep, cleaning workflows, order handoff), meaning skill premiums compress even if jobs remain.

3.5 The Mid‑Market Squeeze: The Most Fragile Middle

The most structurally exposed zone is mid‑market operations that:

cannot out‑scale chains on price, speed, or procurement

cannot out‑differentiate premium venues on experience depth

This is why the Dual‑Triangle Model is not merely academic: it predicts a shrinking middle and intensified competition for small operators who have not moved “up” or “systemized.”

4. Why Premium Dining Becomes More Valuable — and More Human‑Intensive

Premium dining does not win by being “more efficient.” It wins by delivering what cannot be replicated cheaply: experience, meaning, and mastery.

The National Restaurant Association’s 2025 State of the Restaurant Industry highlights that 64% of full‑service customers say the dining experience is more important than price. It also notes that a majority of operators prioritize building on‑premises business—including 90% of fine dining operators and 87% of casual dining operators—over off‑premises growth.

This data supports a clear claim: in premium and experience‑led segments, experience is the growth variable.

4.1 What “Experience” Actually Means Operationally

Experience is not décor alone. It is a professional delivery system:

taste judgment and consistency under real service pressure

craft technique that produces identifiable signature outcomes

aesthetic composition (plating, pacing, sequencing, textures)

service choreography (timing, explanation, pairing, emotional resonance)

storycraft (place, cuisine lineage, technique logic, cultural meaning)

organizational discipline (training systems, QC checkpoints, safety and compliance)

These are precisely the capabilities that do not collapse into SOPs easily—and that compound with mastery.

5. The Strategic Opportunity for Chinese Cuisine

Chinese cuisine has a structural advantage: depth, diversity, regional specificity, and technique richness. But globally it has suffered from an inconsistent premium narrative: abundant supply does not automatically produce premium consensus.

The solution is not marketing slogans. It is professionalization—making the value legible and auditable.

5.1 A Five‑Layer Value Stack for Premium Chinese Cuisine

Premium Chinese cuisine becomes priceable when it consistently delivers multiple layers:

Technique value: heat control, knife work, texture mastery, complex flavor structure

Systems value: station design, prep cadence, training discipline, QC, safety and compliance

Aesthetic value: plating, ceramics, space, pacing and sequence

Service value: explanation, pairing, guidance, hospitality orchestration

Cultural value: regional lineage, history, technique logic, narrative translation

Low‑end competition usually fights on layer (1) alone—often not even that, but “portion and price.” Premium positioning requires stable delivery of (2)–(5).

6. ICC’s Strategic Position: Build the Professional Infrastructure, Not Just “Training”

Under the Dual‑Triangle Model, ICC should not act as a trend commentator. It should operate as industry infrastructure for Chinese culinary professionalization:

6.1 Define: Make “Professional Chinese Chef” a Measurable Standard

ICC can formalize a competency architecture that converts “talent” from a subjective claim into an evaluated structure:

Craft (Technique): mastery under constraints; consistency metrics

Operational Systems: station engineering, cadence, QC checkpoints, food safety

Leadership: training others, managing teams, building repeatable kitchens

Experience Design: sequencing, hospitality pacing, aesthetic coherence

Business Literacy: menu engineering, cost structure, procurement logic, brand translation

The strategic value is not academic. It is market‑making: employers can hire with confidence; consumers can understand pricing; professionals can plan careers.

6.2 Train: Teach “High‑Standard Delivery,” Not “More Recipes”

A premium future rewards chefs who can deliver under pressure with repeatability. Training should therefore be evaluated by:

consistency (variance under service conditions)

reproducibility (team‑based station delivery, not solo performance)

explainability (why techniques work, not just that they work)

trainability (ability to build and transmit standards)

compliance readiness (safety, sanitation, labor discipline)

6.3 Certify & Honor: Blue Banner as Scarce, Auditable, Portable Credibility

If Blue Banner™ is positioned as an honor and standard symbol, its strategic value depends on three properties:

Scarcity → authority

Auditability → trust

Portability → the credential travels with the professional across kitchens, cities, and markets

In a world where career value concentrates upward, the scarce resource is not “people who can cook,” but professionals whose competence can be trusted at premium standards.

7. The Window Narrows at the Base; It Opens at the Top

The Dual‑Triangle Model produces a blunt but actionable conclusion:

Low‑end dining will remain huge in demand, but it will increasingly be operated as a system—more standardized, more automated, more chain‑optimized—compressing individual skill premiums.

Premium dining becomes more valuable because it concentrates on‑premises experience and the “irreducibly human” components of hospitality—where professional talent is the core asset.

Chinese cuisine’s premium opportunity is unlocked by professional infrastructure: standards, training systems, and credible honors.

ICC’s strategic job is therefore not to compete in the low‑end automation race, but to own the premium professionalization frontier—turning Chinese cuisine into a globally legible, professionally certified, experience‑priced category.

References (Public Sources)

California Department of Industrial Relations — Fast Food Minimum Wage FAQ (AB 1228)

Chipotle Newsroom — “Chipotle Debuts Autocado and the Augmented Makeline by Hyphen in Restaurants” (Sep 16, 2024)

James Beard Foundation — 2025 Independent Restaurant Industry Report (with Deloitte)

National Restaurant Association — State of the Restaurant Industry 2025 (key findings)

International Federation of Robotics — “Service Robots See Global Growth Boom” (World Robotics 2025 Service Robots)

Technomic — “Top 500 chain restaurant sales growth slows to 3% in 2024…” (2025 Top 500 Chain Restaurant Report press release)

McKinsey Global Institute — “A Future That Works: Automation, Employment, and Productivity” (In Brief)

Restaurant Dive — Sweetgreen Infinite Kitchen tests (robot kitchens yielding higher tickets; 2024 expansion plans)